Could a Blind Algorithm be Better Than Brazilian Regulators?

An Essay on Unsupervised Machine Learning and Corporate Fraud in Brazil

In January 2023, Brazil woke up to a financial apocalipse. What had long been treated as one of the country’s most emblematic retail champions suddenly disclosed accounting inconsistencies that would later be measured in the tens of billions of reais. Creditors froze lines, equity holders were wiped out in days of all value, and the firm entered judicial reorganization in what quickly became one of the largest corporate collapses in Brazilian history. The name at the center of the storm was Americanas S.A.

In the immediate aftermath, the public debate followed a very predictable script. Commentators asked how such a large discrepancy could have gone unnoticed. Analysts revisited old earnings calls in search of missed clues. Politicians demanded accountability and more regulation. Regulators pointed to disclosure rules and missed information. Auditors emphasized procedures and technical standards. The Brazilian SEC, the Comissão de Valores Mobiliários (CVM), initiated formal inquiries. The company’s long-time external auditor, KPMG, found itself under intense scrutiny.

Yet beneath the legal arguments and institutional defenses lies a simpler and more uncomfortable question: Americanas’ accounting information was public and audited, so how could no regulator or major market player have seen this before?! Where were the alarm systems? Was anyone really watching?

I then decided to test a simple question: Would a blind machine, with no information about Americanas, make the same mistake?

I decided to approach this question without privileged information, whistleblower testimony, or ex post labels of fraud through an unsupervised machine learning system. I used only what any investor, analyst, or regulator could have accessed at the time: published financial statements. I constructed a balanced panel of eleven Brazilian listed companies over the period 2013–2022, yielding 87 firm-year observations after data cleaning. The sample included large retailers such as Magazine Luiza S.A. and other comparably visible firms.

From each firm-year was extracted four financial ratios designed to capture the interaction between leverage, financing costs, and operating performance. The first was the short-term debt ratio, measuring current financial obligations relative to assets. The second was the long-term debt ratio, capturing the structural weight of non-current liabilities. The third variable, which I called “financial weight,” proxied the burden of financial expenses relative to operating scale. The fourth, “implicit margin,” approximated profitability net of financial costs. These are not exotic constructs. They are the kind of ratios routinely calculated in introductory corporate finance courses.

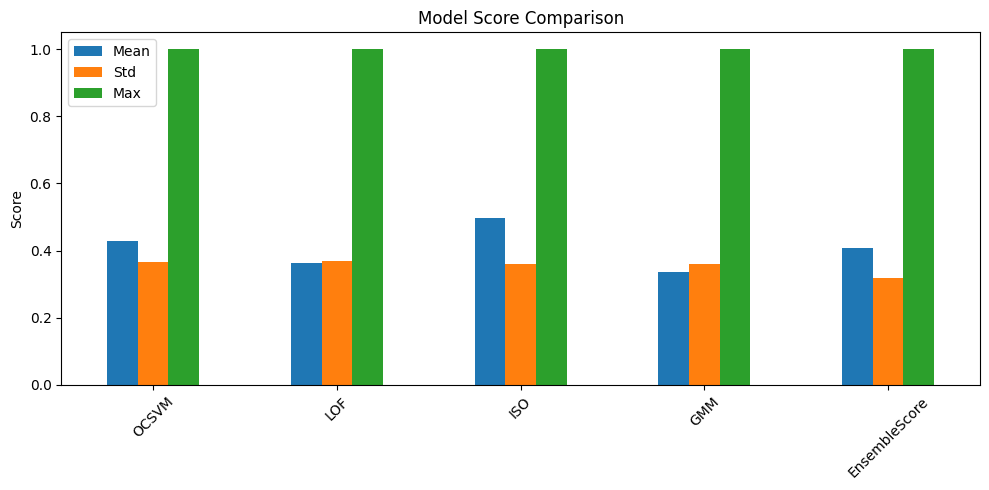

Instead of asking the model to predict fraud, I asked it a more modest question: which observations look statistically unusual relative to the rest of the cross-section and over time? To answer this, I employed four standard unsupervised anomaly detection techniques: One-Class SVM, Local Outlier Factor, Isolation Forest, and Gaussian Mixture Models. Each method captures abnormality from a different geometric or probabilistic perspective. One-Class SVM learns the boundary of “normality” in feature space. LOF evaluates local density deviations. Isolation Forest isolates observations via recursive partitioning. Gaussian mixtures assess likelihood under estimated distributional regimes.

I then aggregated their outputs into a normalized Ensemble Score between zero and one, where higher values indicate greater statistical abnormality. This aggregation reduces method-specific noise and emphasizes consensus signals across techniques.

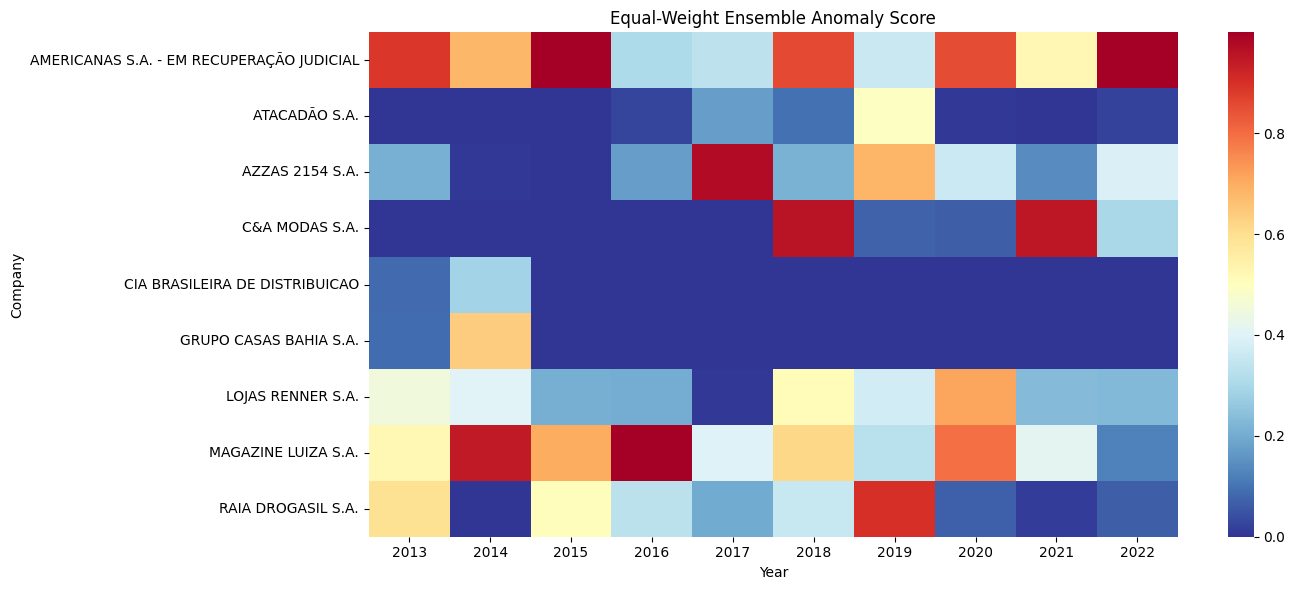

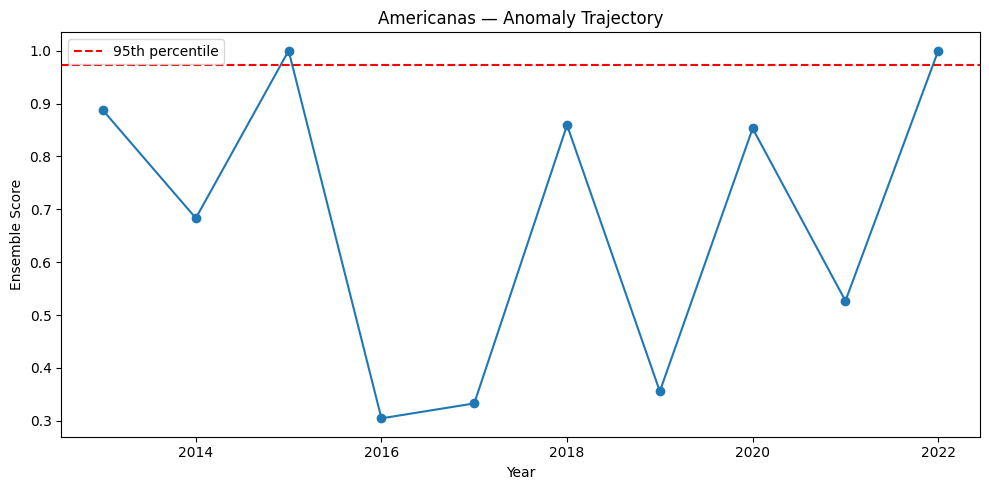

The results are difficult to ignore. Across the full 2013–2022 sample, Americanas S.A. exhibits the highest average Ensemble Score of all firms in the dataset, with a mean score of 0,680. By contrast, the dataset average across all eleven companies is 0,406, and the second-highest average score, that of Magazine Luiza S.A, is 0,584. Not only is Americanas materially higher than the cross-sectional mean, it also maintains a persistent lead over its closest peer across the decade.

More strikingly, in 2015 all four independent algorithms simultaneously assigned Americanas S.A. the maximum anomaly score of 1 within the cross-section. This was the only instance in the entire dataset of 87 firm-year observations in which every method unanimously classified a firm-year as extreme. At the time, there was no public scandal narrative: earnings calls were proceeding normally and credit markets were open. Yet, in purely statistical terms, the configuration of leverage and financial burden relative to margins was an outlier.

One could argue that such a signal might be noise. And indeed, that is precisely what we see with Magazine Luiza S.A. Magalu also received a high anomaly score in one year of the sample, peaking at a perfect ensemble score in 2016, but its subsequent years returned to values much closer to the cross-sectional norm. That pattern is consistent with a transient structural shift tied to aggressive expansion and investment in e-commerce and digital channels, not persistent financial inconsistency.

In the case of Americanas, however, unlike Magazine Luiza’s temporary excursion, the elevated anomaly scores do not dissipate after a single year; they cluster repeatedly across multiple years, and in 2022 they rise again to cross statistically significant thresholds. The persistence of high anomaly scores across many periods strengthens the interpretation that this is not merely random noise or transitory operational dynamics, but rather a structural departure from peer norms that survives across time.

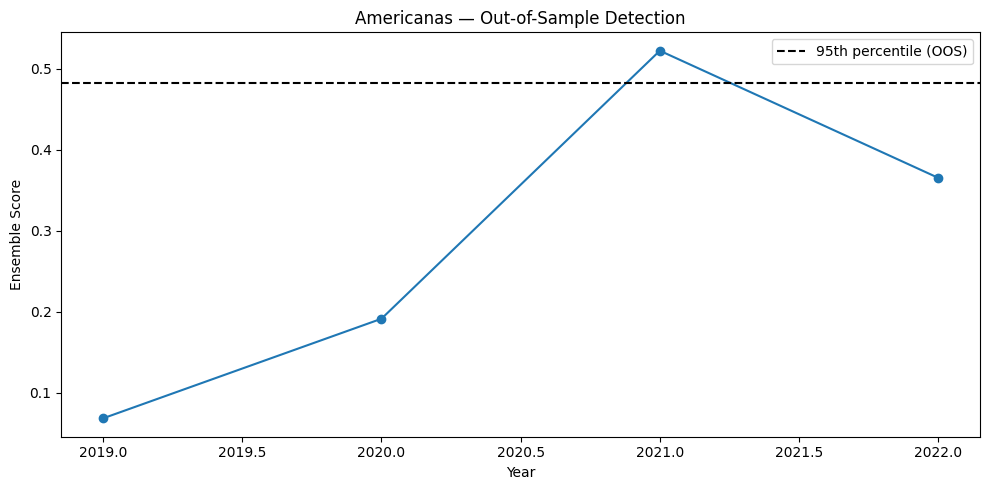

One might argue that such findings are contaminated by hindsight, that the model, having seen the entire sample including the crisis years, is merely overfitting to what we now know. To address this concern, I conducted an out-of-sample exercise. I trained the ensemble exclusively on data from 2013–2018 and then applied it blindly to the period 2019–2022. This simulates a real-time monitoring environment in which the future is unknown at the moment of estimation.

The trajectory that emerges from the out-of-sample test is very revealing. Using only data up to 2018 to define what “normal” looks like, Americanas S.A.’s anomaly score in 2019 was 0.07, a level comfortably within historical norms and well below typical alert thresholds. In 2020, the score rose to 0.19, but it still remained below the empirical 95th-percentile cutoff. Then, in 2021, the anomaly score jumped sharply to 0.52, crossing the 95th percentile alert threshold of approximately 0.48, based solely on the training distribution. In other words, a backward-looking system that learned normality only from 2013–2018 would have generated a statistically significant abnormality signal for Americanas in 2021, a full year before the public disclosure that detonated the market in January 2023.

It is important to emphasize what this does and does not mean. An anomaly score is not a legal verdict. Statistical abnormality can arise from aggressive expansion, strategic restructuring, or temporary shocks. High scores, as said, are signals for investigation, not convictions of wrongdoing.

However, the presence of false positives does not negate the informational value of persistent, multi-method outliers. Financial supervision, by its nature, operates under uncertainty. Regulators do not need certainty of fraud to justify deeper scrutiny. They require structured, defensible criteria for allocating limited investigative resources. An unsupervised anomaly framework provides precisely that: a transparent, replicable filter highlighting firm-year observations whose financial architecture deviates materially from peers and historical patterns. It is a alarm system.

The broader implication concerns institutional design. The CVM already receives standardized financial statements. Computational costs for running anomaly detection on a few dozen ratios across listed firms are trivial relative to the scale of capital markets. An automated system could compute cross-sectional anomaly percentiles quarterly, generating a prioritized review list. Firms breaching a pre-specified threshold could be asked to provide additional reconciliations or clarifications. Such a mechanism would not replace audits or enforcement; it would complement them with systematic statistical surveillance.

The Americanas case is therefore not merely a story of accounting irregularities. It is a test of whether modern financial oversight incorporates the analytical tools already commonplace in other domains. Banks deploy anomaly detection for anti-money laundering. E-commerce platforms use it to flag fraudulent transactions in milliseconds. Yet capital market supervision often remains anchored in reactive, complaint-driven processes.

What my experiment suggests is unsettling in its simplicity. Using four ordinary financial ratios and off-the-shelf unsupervised algorithms, one can generate a persistent abnormality signal for a major listed corporation years before its collapse becomes public knowledge. The data were not hidden. The mathematics were not exotic. The exercise required no privileged access, only attention!

SUMMARY

Mean Std Max

OCSVM 0.428492 0.366618 1.0

LOF 0.364271 0.368413 1.0

ISO 0.496863 0.359368 1.0

GMM 0.335726 0.359503 1.0

EnsembleScore 0.406338 0.316968 1.0

SCORES BY COMPANY

OCSVM \

mean std max

Company

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.650567 0.347789 1.000000

ATACADÃO S.A. 0.146696 0.216800 0.525246

AZZAS 2154 S.A. 0.362614 0.370920 1.000000

C&A MODAS S.A. 0.368502 0.507654 1.000000

CIA BRASILEIRA DE DISTRIBUICAO 0.000000 0.000000 0.000000

GRUPO CASAS BAHIA S.A. 0.467542 0.331480 0.701933

LOJAS RENNER S.A. 0.466044 0.336330 1.000000

MAGAZINE LUIZA S.A. 0.680101 0.353722 1.000000

RAIA DROGASIL S.A. 0.272699 0.212763 0.603291

LOF \

mean std max

Company

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.672959 0.304590 1.000000

ATACADÃO S.A. 0.091900 0.132019 0.334412

AZZAS 2154 S.A. 0.245252 0.331717 1.000000

C&A MODAS S.A. 0.493511 0.463873 1.000000

CIA BRASILEIRA DE DISTRIBUICAO 0.397358 0.351665 0.646022

GRUPO CASAS BAHIA S.A. 0.516361 0.683970 1.000000

LOJAS RENNER S.A. 0.188829 0.209620 0.602501

MAGAZINE LUIZA S.A. 0.474465 0.396270 1.000000

RAIA DROGASIL S.A. 0.324921 0.404170 1.000000

ISO \

mean std max

Company

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.789961 0.284164 1.000000

ATACADÃO S.A. 0.089793 0.153225 0.364466

AZZAS 2154 S.A. 0.331454 0.326677 0.903569

C&A MODAS S.A. 0.515821 0.430864 0.994818

CIA BRASILEIRA DE DISTRIBUICAO 0.301872 0.153886 0.410686

GRUPO CASAS BAHIA S.A. 0.255533 0.361378 0.511066

LOJAS RENNER S.A. 0.453431 0.203289 0.696127

MAGAZINE LUIZA S.A. 0.778788 0.295212 1.000000

RAIA DROGASIL S.A. 0.493032 0.367997 1.000000

GMM \

mean std max

Company

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.607847 0.413202 1.000000

ATACADÃO S.A. 0.142162 0.320552 0.860090

AZZAS 2154 S.A. 0.322443 0.333713 1.000000

C&A MODAS S.A. 0.500603 0.481001 1.000000

CIA BRASILEIRA DE DISTRIBUICAO 0.042857 0.060608 0.085713

GRUPO CASAS BAHIA S.A. 0.213925 0.191231 0.349146

LOJAS RENNER S.A. 0.221921 0.241298 0.701915

MAGAZINE LUIZA S.A. 0.402049 0.377845 1.000000

RAIA DROGASIL S.A. 0.251986 0.308866 1.000000

EnsembleScore

mean std max

Company

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.680333 0.278797 1.000000

ATACADÃO S.A. 0.117638 0.176859 0.493366

AZZAS 2154 S.A. 0.315441 0.307171 0.975892

C&A MODAS S.A. 0.469609 0.452420 0.959331

CIA BRASILEIRA DE DISTRIBUICAO 0.185522 0.141540 0.285605

GRUPO CASAS BAHIA S.A. 0.363340 0.392015 0.640536

LOJAS RENNER S.A. 0.332556 0.199407 0.712244

MAGAZINE LUIZA S.A. 0.583851 0.280224 1.000000

RAIA DROGASIL S.A. 0.335660 0.292409 0.900823

SCORES BY YEAR

OCSVM LOF ISO \

mean std max mean std max mean std

Year

2013 0.418289 0.322194 1.0 0.365544 0.391762 1.0 0.489863 0.362371

2014 0.390564 0.391774 1.0 0.638465 0.363106 1.0 0.590415 0.375478

2015 0.431269 0.393211 1.0 0.489296 0.451463 1.0 0.598477 0.396452

2016 0.408501 0.329696 1.0 0.312808 0.365926 1.0 0.378664 0.366920

2017 0.230521 0.381589 1.0 0.325607 0.380434 1.0 0.549333 0.365477

2018 0.576945 0.333324 1.0 0.366030 0.379547 1.0 0.594343 0.438269

2019 0.621463 0.346826 1.0 0.340924 0.320297 1.0 0.471757 0.334469

2020 0.391246 0.410400 1.0 0.430033 0.387270 1.0 0.460777 0.394882

2021 0.526447 0.461903 1.0 0.158044 0.372970 1.0 0.473670 0.381298

2022 0.253916 0.339295 1.0 0.277978 0.352519 1.0 0.394340 0.367192

GMM EnsembleScore

max mean std max mean std max

Year

2013 1.0 0.344905 0.326957 1.0 0.404650 0.295727 0.887145

2014 1.0 0.358628 0.363659 1.0 0.494518 0.331228 0.944470

2015 1.0 0.413572 0.393349 1.0 0.483154 0.395709 1.000000

2016 1.0 0.254902 0.372254 1.0 0.338719 0.341394 1.000000

2017 1.0 0.283841 0.359737 1.0 0.347325 0.336692 0.975892

2018 1.0 0.522026 0.390809 1.0 0.514836 0.321421 0.959331

2019 1.0 0.399150 0.418216 1.0 0.458324 0.268424 0.900823

2020 1.0 0.351171 0.371386 1.0 0.408307 0.373332 0.853037

2021 1.0 0.144395 0.377307 1.0 0.325639 0.337225 0.949575

2022 1.0 0.291224 0.348862 1.0 0.304365 0.333124 1.000000

TOP 3 ANOMALIES PER YEAR

OCSVM LOF ISO \

Year Company

2013 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 1.000000 0.824764 0.723815

MAGAZINE LUIZA S.A. 0.438079 0.283657 1.000000

RAIA DROGASIL S.A. 0.224851 1.000000 0.724619

2014 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.329720 0.919018 0.973483

GRUPO CASAS BAHIA S.A. 0.701933 1.000000 0.511066

MAGAZINE LUIZA S.A. 1.000000 0.777881 1.000000

2015 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 1.000000 1.000000 1.000000

MAGAZINE LUIZA S.A. 0.522353 0.905767 0.789289

RAIA DROGASIL S.A. 0.510125 0.421568 0.792434

2016 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.254174 0.419052 0.334400

MAGAZINE LUIZA S.A. 1.000000 1.000000 1.000000

RAIA DROGASIL S.A. 0.371901 0.238765 0.592560

2017 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.107622 0.529968 0.493496

AZZAS 2154 S.A. 1.000000 1.000000 0.903569

MAGAZINE LUIZA S.A. 0.166951 0.195143 1.000000

2018 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.721751 0.804047 1.000000

C&A MODAS S.A. 0.842508 1.000000 0.994818

MAGAZINE LUIZA S.A. 1.000000 0.266251 0.966645

2019 ATACADÃO S.A. 0.525246 0.334412 0.253718

AZZAS 2154 S.A. 1.000000 0.349182 0.793928

RAIA DROGASIL S.A. 0.603291 1.000000 1.000000

2020 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.642353 0.769797 1.000000

LOJAS RENNER S.A. 1.000000 0.602501 0.696127

MAGAZINE LUIZA S.A. 0.777304 1.000000 0.840054

2021 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 1.000000 0.096983 1.000000

C&A MODAS S.A. 1.000000 1.000000 0.798301

MAGAZINE LUIZA S.A. 1.000000 0.008839 0.642220

2022 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 1.000000 1.000000 1.000000

AZZAS 2154 S.A. 0.258614 0.471537 0.494063

C&A MODAS S.A. 0.000000 0.127538 0.654811

GMM EnsembleScore Rank

Year Company

2013 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 1.000000 0.887145 1.0

MAGAZINE LUIZA S.A. 0.365284 0.521755 3.0

RAIA DROGASIL S.A. 0.416519 0.591497 2.0

2014 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.511251 0.683368 2.0

GRUPO CASAS BAHIA S.A. 0.349146 0.640536 3.0

MAGAZINE LUIZA S.A. 1.000000 0.944470 1.0

2015 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 1.000000 1.000000 1.0

MAGAZINE LUIZA S.A. 0.593730 0.702785 2.0

RAIA DROGASIL S.A. 0.304841 0.507242 3.0

2016 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.211479 0.304776 3.0

MAGAZINE LUIZA S.A. 1.000000 1.000000 1.0

RAIA DROGASIL S.A. 0.111936 0.328791 2.0

2017 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.200888 0.332994 3.0

AZZAS 2154 S.A. 1.000000 0.975892 1.0

MAGAZINE LUIZA S.A. 0.230820 0.398228 2.0

2018 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.911387 0.859296 2.0

C&A MODAS S.A. 1.000000 0.959331 1.0

MAGAZINE LUIZA S.A. 0.221170 0.613516 3.0

2019 ATACADÃO S.A. 0.860090 0.493366 3.0

AZZAS 2154 S.A. 0.603378 0.686622 2.0

RAIA DROGASIL S.A. 1.000000 0.900823 1.0

2020 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 1.000000 0.853037 1.0

LOJAS RENNER S.A. 0.550350 0.712244 3.0

MAGAZINE LUIZA S.A. 0.557201 0.793640 2.0

2021 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.010633 0.526904 2.0

C&A MODAS S.A. 1.000000 0.949575 1.0

MAGAZINE LUIZA S.A. 0.000129 0.412797 3.0

2022 AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 1.000000 1.000000 1.0

AZZAS 2154 S.A. 0.338167 0.390595 2.0

C&A MODAS S.A. 0.414832 0.299295 3.0

CORRELATION MATRIX

OCSVM LOF ISO GMM EnsembleScore

OCSVM 1.000000 0.542507 0.708175 0.629502 0.826020

LOF 0.542507 1.000000 0.706495 0.817546 0.879511

ISO 0.708175 0.706495 1.000000 0.682112 0.886920

GMM 0.629502 0.817546 0.682112 1.000000 0.896473

EnsembleScore 0.826020 0.879511 0.886920 0.896473 1.000000

Financial Ratios – Global Summary:

ShortTermDebtRatio LongTermDebtRatio FinancialWeight ImplicitMargin

count 87.000000 87.000000 87.000000 87.000000

mean 0.492931 0.366103 -1.665897 4.101233

std 0.166644 0.203898 31.066566 35.753431

min 0.133464 0.000000 -270.429869 -33.493163

25% 0.373282 0.194642 -0.829335 0.672482

50% 0.490561 0.351470 -0.241740 0.724586

75% 0.645540 0.533814 -0.080817 0.800592

max 0.763093 0.753203 85.987066 331.996973

Financial Ratios By Company:

ShortTermDebtRatio \

mean std

DENOM_CIA

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.588199 0.160728

ATACADÃO S.A. 0.566495 0.062214

AZZAS 2154 S.A. 0.345763 0.062235

C&A MODAS S.A. 0.489694 0.071354

CIA BRASILEIRA DE DISTRIBUICAO 0.500831 0.035020

FERTILIZANTES HERINGER S.A. 0.417351 0.028991

GRUPO CASAS BAHIA S.A. 0.422589 0.016354

LOJAS RENNER S.A. 0.264083 0.051271

MAGAZINE LUIZA S.A. 0.625436 0.120393

RAIA DROGASIL S.A. 0.683826 0.041839

\

min max count

DENOM_CIA

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.133464 0.763093 13

ATACADÃO S.A. 0.441755 0.622417 7

AZZAS 2154 S.A. 0.242312 0.437987 13

C&A MODAS S.A. 0.387897 0.580002 5

CIA BRASILEIRA DE DISTRIBUICAO 0.465052 0.558621 5

FERTILIZANTES HERINGER S.A. 0.384422 0.439032 3

GRUPO CASAS BAHIA S.A. 0.403345 0.447891 5

LOJAS RENNER S.A. 0.221035 0.403432 13

MAGAZINE LUIZA S.A. 0.368215 0.761839 12

RAIA DROGASIL S.A. 0.620164 0.739506 11

LongTermDebtRatio \

mean std

DENOM_CIA

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.586997 0.197783

ATACADÃO S.A. 0.231207 0.074977

AZZAS 2154 S.A. 0.313136 0.178297

C&A MODAS S.A. 0.384717 0.226466

CIA BRASILEIRA DE DISTRIBUICAO 0.403582 0.138624

FERTILIZANTES HERINGER S.A. 0.151965 0.145658

GRUPO CASAS BAHIA S.A. 0.255697 0.128421

LOJAS RENNER S.A. 0.559844 0.111898

MAGAZINE LUIZA S.A. 0.274789 0.149693

RAIA DROGASIL S.A. 0.207225 0.057005

\

min max count

DENOM_CIA

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 0.000000 0.753203 13

ATACADÃO S.A. 0.097449 0.297693 7

AZZAS 2154 S.A. 0.014119 0.590688 13

C&A MODAS S.A. 0.002378 0.604675 5

CIA BRASILEIRA DE DISTRIBUICAO 0.190447 0.513102 5

FERTILIZANTES HERINGER S.A. 0.003206 0.294311 3

GRUPO CASAS BAHIA S.A. 0.067058 0.401498 5

LOJAS RENNER S.A. 0.343334 0.713084 13

MAGAZINE LUIZA S.A. 0.002298 0.422591 12

RAIA DROGASIL S.A. 0.135239 0.333551 11

FinancialWeight \

mean std

DENOM_CIA

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL 8.029745 23.689426

ATACADÃO S.A. -0.632425 0.510583

AZZAS 2154 S.A. -0.310498 0.481168

C&A MODAS S.A. -51.453633 122.567138

CIA BRASILEIRA DE DISTRIBUICAO -1.373693 0.612077

FERTILIZANTES HERINGER S.A. 12.091665 28.079391

GRUPO CASAS BAHIA S.A. -0.960372 3.556037

LOJAS RENNER S.A. -0.252193 0.223965

MAGAZINE LUIZA S.A. -0.075469 4.754329

RAIA DROGASIL S.A. -0.364419 0.210991

\

min max count

DENOM_CIA

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL -9.812826 85.987066 13

ATACADÃO S.A. -1.617515 -0.195936 7

AZZAS 2154 S.A. -1.889402 -0.086615 13

C&A MODAS S.A. -270.429869 13.895439 5

CIA BRASILEIRA DE DISTRIBUICAO -2.393520 -0.879407 5

FERTILIZANTES HERINGER S.A. -5.042055 44.497127 3

GRUPO CASAS BAHIA S.A. -5.987552 4.001647 5

LOJAS RENNER S.A. -0.871130 -0.028923 13

MAGAZINE LUIZA S.A. -8.048459 9.487017 12

RAIA DROGASIL S.A. -0.787541 -0.118404 11

ImplicitMargin \

mean std

DENOM_CIA

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL -1.900203 9.493492

ATACADÃO S.A. 0.705206 0.062894

AZZAS 2154 S.A. 0.781682 0.072373

C&A MODAS S.A. 66.816349 148.240810

CIA BRASILEIRA DE DISTRIBUICAO 0.794759 0.097212

FERTILIZANTES HERINGER S.A. 0.553875 0.229583

GRUPO CASAS BAHIA S.A. 0.636987 0.041224

LOJAS RENNER S.A. 0.764396 0.106021

MAGAZINE LUIZA S.A. 0.409617 1.022101

RAIA DROGASIL S.A. 0.786999 0.086804

min max count

DENOM_CIA

AMERICANAS S.A. - EM RECUPERAÇÃO JUDICIAL -33.493163 1.030146 13

ATACADÃO S.A. 0.582712 0.777188 7

AZZAS 2154 S.A. 0.698211 0.893559 13

C&A MODAS S.A. -0.019156 331.996973 5

CIA BRASILEIRA DE DISTRIBUICAO 0.689860 0.894366 5

FERTILIZANTES HERINGER S.A. 0.289199 0.699191 3

GRUPO CASAS BAHIA S.A. 0.585719 0.678575 5

LOJAS RENNER S.A. 0.665683 0.989465 13

MAGAZINE LUIZA S.A. -2.704380 1.122821 12

RAIA DROGASIL S.A. 0.663329 1.005824 11

Definitely a case of "nobody" wanting the see the obvious. As is/was the case with Banco Master, the Fictor SCPs, and many others. Astute market participants were avoiding these traps months (sometimes years) before each crisis came to light. The regulators, no so much.

Absolutely spot-on analysis and conclusion.

This is really great